It is important to anticipate the financial and accounting implications of preparing PPA contracts. There are important differences in the accounting treatment between physical and financial PPA and, in the case of the latter, their accounting can lead to volatility in the income statement. Experts stress the relevance of long-term price forecasts for a reliable and stable valuation of PPA to avoid problems in the viability of the financial statements.

For the fourth time, Deloitte participated in the monthly webinar series hosted by AleaSoft Energy Forecasting and AleaGreen. This was the edition number 37. This collaboration provided energy professionals with valuable insights into the financing and valuation of renewable energy resources. The event attracted considerable interest in both English and Spanish. The full recording of the event is available to AleaSoft Energy Forecasting and Deloitte clients.

To be taken into account during the preparation and negotiation of the PPA

The Deloitte experts’ recommendation during the webinar is to anticipate and consider the financial and accounting implications of PPA (Power Purchase Agreements) from the outset of contract preparation. Based on their extensive experience in negotiating and accounting for PPA contracts, the first step before structuring the contract is to properly define the hedging strategy in a way that meets the hedging objectives and interests of both parties.

It is essential to anticipate all relevant aspects of the PPA in order to be able to react and avoid or mitigate the accounting impact of a financial PPA on the income statement, or to be aware that some of the clauses of a physical PPA may also create volatility in the income statement.

The vast majority of PPA currently signed in Spain are financial and require valuation and fair value calculation if they are accounted for as derivatives. If hedge accounting is applied to them, a number of important requirements must also be met.

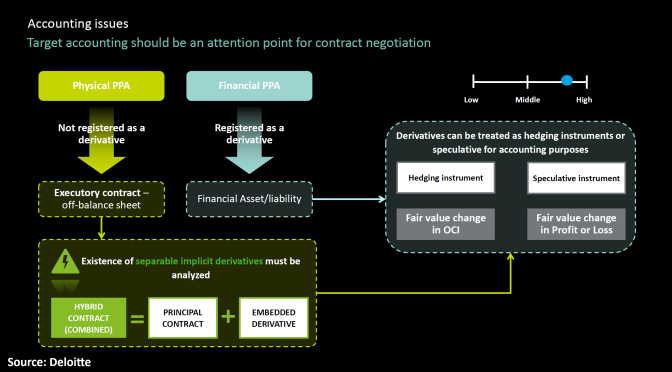

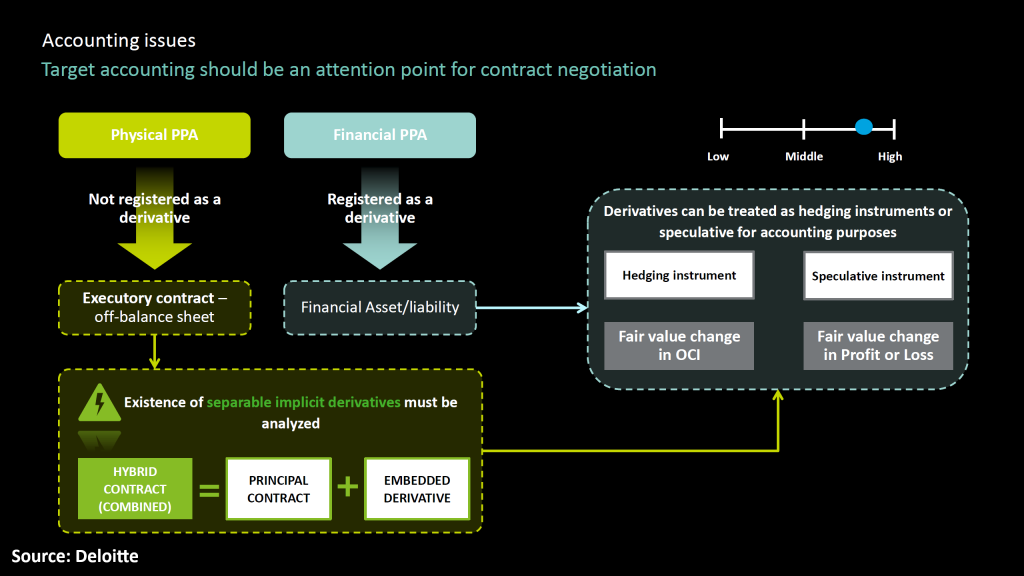

Accounting aspects of physical and financial PPA

When considering a PPA, it is important to bear in mind from the outset that its typology will have an impact on accounting. Physical PPA are usually preferred by both generators and off-takers. A physical PPA is reflected in the income statement as a revenue or an expense, depending on whether the energy is bought or sold.

Financial PPA are registered as derivatives and have more accounting implications that need to be taken into account. A financial PPA is a financial asset or liability with changes in value recognised in the income statement as the market value of the PPA fluctuates. There is also an option to apply hedge accounting to the PPA if a number of conditions are met. Under hedge accounting, changes in the value of the PPA are reflected in the net equity and do not result in volatility in the income statement.

There are also cases where physical PPA contain a clause that may require them to be treated and accounted for as derivatives. This is the case with take?or?pay clauses, which are common in contracts.

Deloitte’s recommendation is to agree with the auditors how the PPA will be treated for accounting purposes at the outset of contract preparation. This will make it possible to anticipate all the implications of any decision taken on the terms and conditions of the contract.

Valuation of PPA

For accounting purposes, financial PPA require a valuation. This valuation should reflect their market value, a fair value, which should be reflected in the income statement.

The valuation of PPA depends on several factors. Swap contracts, with a fixed price, are relatively easy to value by difference from market prices. Option contracts, with a floor or collar rate, require more complex valuation. Valuation will also depend on the profile of the PPA, whether baseload, peak, solar profile or wind profile, which will affect the valuation model.

A key aspect of contract valuation is the data used to calculate market value. According to Deloitte’s experts, there is currently no sufficiently transparent, liquid and observable public long-term price curve that is sufficiently reliable and stable to enable long-term PPA valuations. Deloitte recommends and believes that it is essential to have an advisor to provide long-term price curve forecasts. In addition to the valuation, the price forecasts will allow volatility calculations that will enable the valuation of the PPA if its pricing structure includes options.

In any case, experts insist that if the valuation is done properly and the price forecasts are correct and stable, there should be no problems with the viability of the financial statements.

AleaSoft Energy Forecasting’s analysis on the prospects for energy markets in Europe and the energy transition

The next webinar in the monthly webinar series hosted by AleaSoft Energy Forecasting and AleaGreen is scheduled on Thursday, November 16. This time, the collaboration with AEPIBAL, the Business Association of Batteries and Energy Storage, is confirmed and will explore on energy storage forecasting as a key component in the transition to more sustainable energy sources.