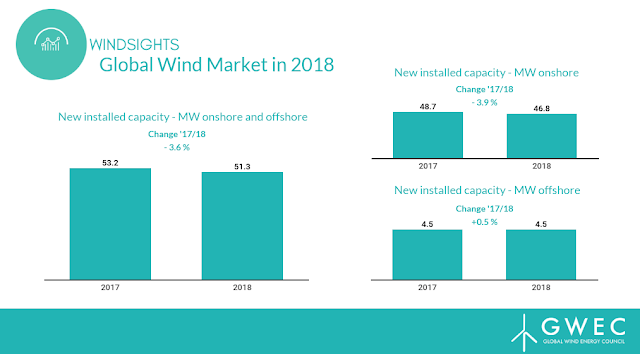

The Global Wind Energy Council has published the 14th edition of the Global Wind Report, the wind power industry’s flagship publication which provides a comprehensive view of the sector. Data in the report confirms that 2018 was a positive year for the wind turbines industry, with 51.3 GW of new wind farm installations. Market-based mechanisms, such as auctions, tenders and Green Certificates were the main drivers behind new installations in 2018.

GWEC expects strong growth in the coming period, with around 300 GW of new capacity to be added in the next five years, as the wind industry continues to prove its cost-competitiveness in relation to incumbent fossil fuel generation and nuclear around the world.

Karin Ohlenforst, Director of Market Intelligence at GWEC, said: “2018 was a good year for the global wind industry, with installations remaining above 50 GW. The dominance of onshore wind power is not surprising given continued and growing investment, with market-based mechanisms like auctions, tenders and Green Certificates being the main drivers of new onshore installations, accounting for 35% of total installations. 2018 was also a pivotal year for the offshore industry, particularly in Asia. If governments remain committed, offshore wind will become a truly global market in the next five years.”

Ben Backwell, CEO of GWEC, said: “We have changed the way we gather, analyse and share data. This year’s Global Wind Report is built on our new and improved Market Intelligence function that offers unmatched exclusive data and insights. We are growing our team and are more dedicated than ever to steering the industry and supporting our members into new and exciting opportunities for wind energy.”

Looking ahead, the market outlook for the global wind industry is strong. GWEC Market Intelligence expects over 300 GW of new capacity to be added in the next five years. In the short term, governmental support, in the form of auction and tender programmes and renewable targets, will continue to be a significant driver for new installations. In addition, opportunities for wind energy to operate on a commercial basis are increasing as the industry continues to prove its cost-competitiveness and bilateral agreements, such as corporate PPAs, grow.

The report identifies three global trends as the main drivers of future market growth, aside from regulation and government targets: changing business models of industry participants, unlocking further volume through corporate procurement outside of mature markets and how value-focused solutions, such as hybrid generation plants, are unlocking more opportunities for the wind industry.

Changing business models of industry stakeholders are driving growth by intensifying competition. Increasing digitalisation opportunities are bringing in new players with new competencies and solutions, whilst a number of traditional players are revising their models to make investments outside of their core business.

Meanwhile, a steady growth in corporate sourcing as large companies choose wind as their main preference for power procurement is driving strong growth in mature wind markets. It has the potential to propel further demand but support from local regulators and authorities is required to make this happen. Taking corporate procurement outside of mature markets can unlock even further volume for wind.

The rising focus on the value an energy source provides to a system and a market, including the produced energy output, is easing integration and helping to match supply and demand. Therefore, in order to develop new solutions for technology, project design and financial structuring, regulatory adjustments are required to account for the added value of energy sources such as wind.

GWEC Market Intelligence uses original data and analysis to compile the report and offers broader insight with individual country profiles, stakeholder insights and thought leadership across all regions to inform members and help facilitate the growth and development of the wind industry.

GWEC, together with key industry stakeholders, is working to increase policy momentum, as well as understanding of the competitiveness of wind energy globally. The strong growth in wind energy generation is making a key contribution to ensuring countries meet their international climate agreement commitments whilst satisfying rising energy demand. It forms a crucial part of the solution to reduce emissions, strengthen energy security, lower costs, and boost investment into local economies.

Appendix:

Regional highlights:

- Asia

- China accounted for the highest proportion of new installations in 2018, both offshore (40%) and onshore (45%).

- Governments of South-East Asian markets like Vietnam and the Philippines have set targets for wind energy deployment to increase installations.

- Indonesia and Thailand have plans in place to decrease reliability on nuclear energy and fossil fuels.

- Latin America

- The Latin American wind market has grown over the past ten years, accumulating total installations of 25 GW.

- Auction and tenders will drive the majority of installations in the Latin American markets. Brazil and Argentina, for example, continue to conduct joint capacity auctions for onshore wind and solar.

- Colombia is an emerging wind market, with the government setting the ambition for 1.5 GW of renewable capacity by 2022.

- Africa and the Middle East

- The majority of onshore installations are expected to come from Egypt, Kenya, Morocco and South Africa, adding over 6 GW new capacity by 2023.

- The highest capacity additions in 2018 came from Egypt with 380 MW, proving the progress of this market.