In the week of February 26, prices in the European electricity markets were higher than in the previous week. The exception was the Iberian market, where prices fell and were the lowest, something that has been happening since February 18. Weekly Iberian wind energy production was the highest since October, which led to the lowest weekly average price ever in Spain. Gas and CO2 prices halted the downward trend and increased compared to the previous week.

Solar photovoltaic, solar thermoelectric and wind energy production

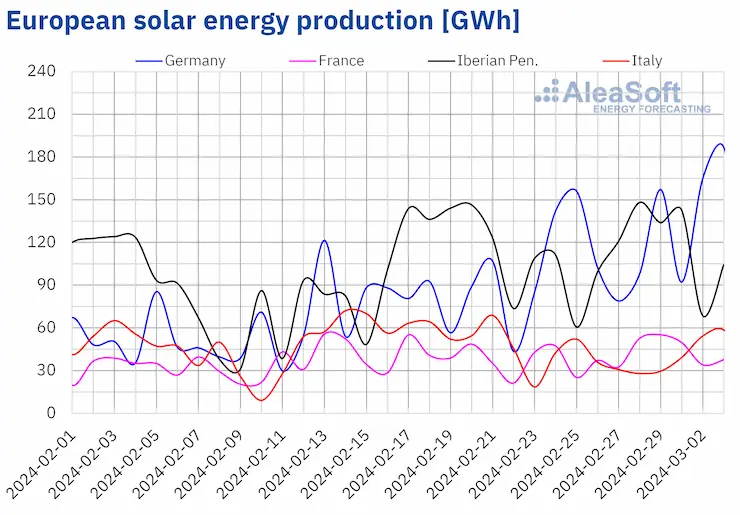

In the week of February 26, solar energy production increased in most major European electricity markets compared to the previous week, continuing the upward trend for the third consecutive week. Increases ranged from 6.1% in Spain to 30% in Germany. France, with a 15% increase, reversed the previous week’s drop. Italy, on the other hand, registered a 17% drop in solar energy production for the second consecutive week.

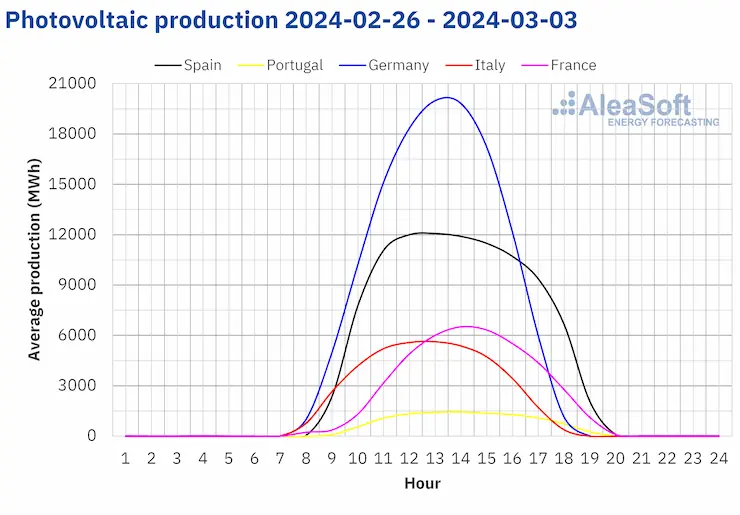

With the arrival of spring and the increase in daylight hours, daily photovoltaic energy production in some markets returned to levels last seen in autumn. On February 28, the Portuguese market generated 14 GWh, the highest value since the end of September and also the highest value ever registered for a February month, breaking the previous record of February 20 when generation reached 13 GWh. The German and Spanish markets also registered the highest solar energy production since October, with 187 GWh generated on March 3 in Germany and 119 GWh generated on March 1 in Spain.

For the week of March 4, according to AleaSoft Energy Forecasting’s solar energy production forecasts, this week’s upward trend will continue in Germany and Italy. However, the Spanish market will register a decrease in solar energy production compared to the previous week.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE and TERNA.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE and TERNA.

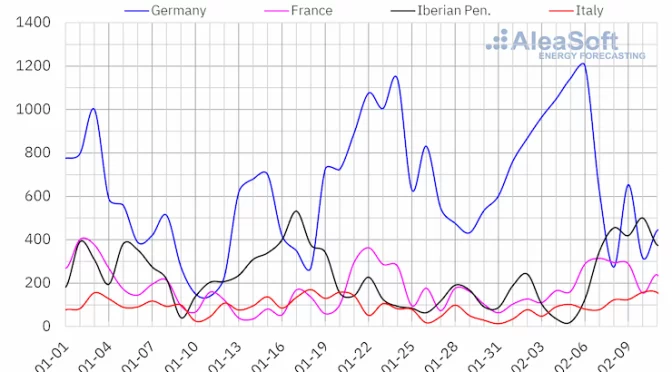

In the week of February 26, wind energy production increased for the second consecutive week in the Iberian Peninsula and Italy. In both cases the increase was 11%. The German and French markets reversed the upward trend of the previous week and registered production decreases of 47% and 12%, respectively.

Strong wind on the Iberian Peninsula brought weekly production to levels last seen in late October. During the week of February 26, the Spanish market generated 2102 GWh using this technology and the Portuguese market generated 546 GWh.

For the week of March 4, AleaSoft Energy Forecasting’s wind energy production forecasts indicate an increase in Italy and Germany, while in France and the Iberian Peninsula it will decrease.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE and TERNA.

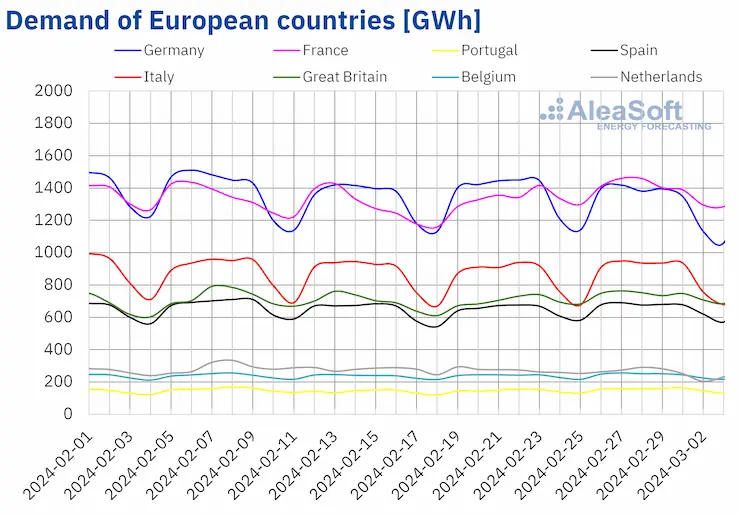

Electricity demand

In the week of February 26, electricity demand increased for the second consecutive week in most major European electricity markets compared to the previous week. The Portuguese market registered the largest increase, 5.7%. The Belgian, Spanish and Italian markets registered the smallest increase, 2.0% each, with Italy reversing the previous week’s downward trend. Demand declined only in the Dutch and German markets, by 5.3% and 4.0% respectively. This was the third consecutive weekly decline for the Netherlands, while Germany reversed last week’s trend.

The increase in demand was related to the drop in average temperatures. In most analyzed European markets, average temperatures for the week fell between 0.6 °C and 1.7 °C compared to the previous week. The exception was Italy, where average temperatures increased by 0.4 °C.

For the week of March 4, according to AleaSoft Energy Forecasting’s demand forecasts, the upward trend will continue and demand will increase in Belgium and the Iberian Peninsula. In Germany and the Netherlands, demand will also rise, reversing the previous week’s drop. In contrast, France, Italy and Great Britain will register a drop in demand.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE, TERNA, National Grid and ELIA.

European electricity markets

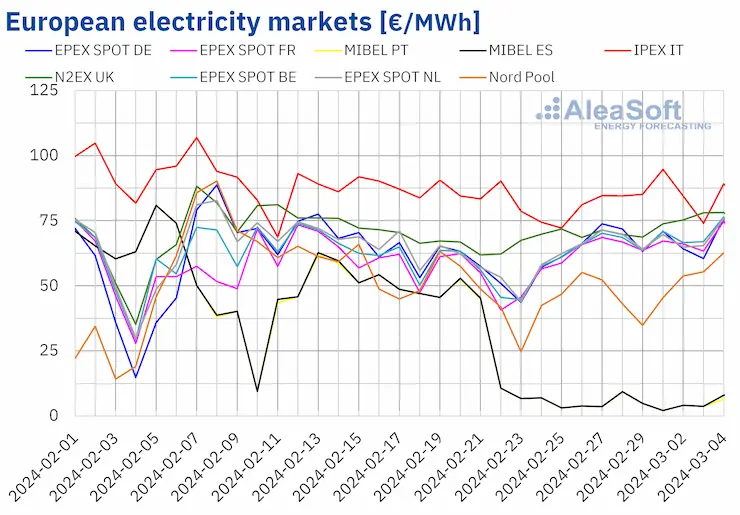

After the recovery registered in the last days of the previous week, during the week of February 26, prices in the main European electricity markets oscillated, registering averages higher than those of the previous week in most cases. The exception was the MIBEL market of Spain and Portugal, with a fall of 81%. The EPEX SPOT market of Belgium and France reached the largest rise, 21%. On the other hand, the IPEX market of Italy and the Nord Pool market of the Nordic countries registered the smallest increases, 2.5% and 4.5%, respectively. In the rest of the markets analyzed at AleaSoft Energy Forecasting, prices increased between 8.2% in the N2EX market of the United Kingdom and 18% in the EPEX SPOT market of Germany.

In the last week of February, weekly averages were below €70/MWh in most analyzed European electricity markets. The exceptions were the British market, with an average of €72.22/MWh, and the Italian market, with an average of €84.11/MWh. In contrast, the Portuguese and Spanish markets registered the lowest weekly prices, €4.52/MWh and €4.53/MWh, respectively. These prices were the lowest ever in the Spanish market and the second lowest in the Portuguese market. In the rest of the analyzed markets, prices ranged from €48.57/MWh in the Nordic market to €67.56/MWh in the Belgian market.

Since February 18, the MIBEL market has consecutively registered the lowest daily prices among the main European electricity markets. During the week of February 26, this market registered 73 hours with prices below €1/MWh. Of these, there were 44 hours with a price of €0/MWh, fourteen of which registered on Sunday, March 3. On that Sunday, high levels of renewable wind and solar energy production combined with the low demand usual for this day of the week.

During the week of February 26, the increase in the average price of gas and CO2 emission rights and the increase in demand in most analyzed markets led to higher prices in the European electricity markets. The decline in wind energy production in markets such as Germany and France also contributed to this behavior. However, the increase in wind and solar energy production on the Iberian Peninsula resulted in significant price decreases in the MIBEL market.

AleaSoft Energy Forecasting’s price forecasts indicate that in the first week of March, European electricity markets prices might continue to rise. In the case of the MIBEL market, prices might also start to recover in that week. The increase in demand and the fall in wind energy production in most markets will lead to this behavior. The drop in solar energy production in the Spanish market will also contribute to price rises in this market.

Source: Prepared by AleaSoft Energy Forecasting using data from OMIE, EPEX SPOT, Nord Pool and GME.

Brent, fuels and CO2

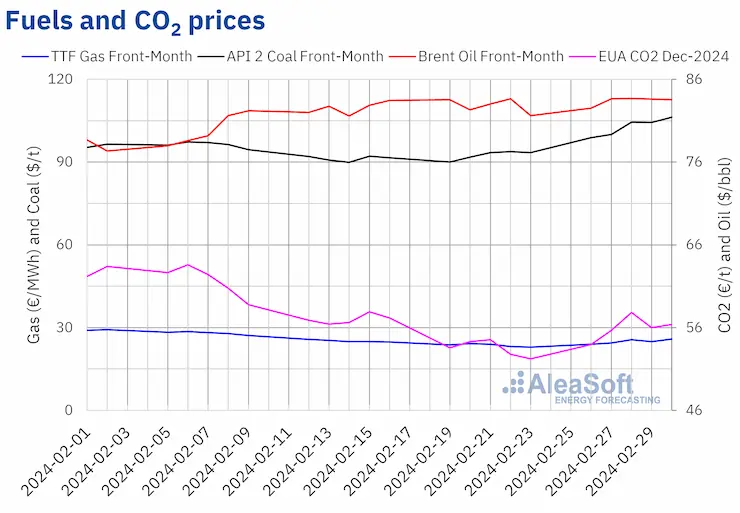

In the last week of February, Brent oil futures for the Front?Month in the ICE market registered their weekly minimum settlement price, $82.53/bbl, on Monday, February 26. In the first three sessions of the week, prices increased and on Wednesday, February 28, they reached the weekly maximum settlement price, $83.68/bbl. This price was the highest since the first half of November 2023. In the last sessions of the week, prices remained stable. On Friday, March 1, the settlement price was $83.55/bbl, 2.4% higher than on Friday of the previous week.

In the last week of February, expectations about the continuation of OPEC+ production cuts in the next quarter contributed to keep settlement prices above $83/bbl in almost every session of the week.

Production cut announcements made at the end of the week by Russia and other OPEC+ member countries might have an upward influence on Brent prices in the first week of March.

As for TTF gas futures in the ICE market for the Front?Month, on Monday, February 26, they reached the weekly minimum settlement price, €24.01/MWh. During the last week of February, prices increased in almost all sessions. As a result, on Friday, March 1, these futures registered their weekly maximum settlement price, €25.81/MWh. According to data analyzed at AleaSoft Energy Forecasting, this price was 13% higher than the previous Friday.

Forecasts of low temperatures and lower wind energy production contributed to the increase in TTF gas futures prices, as well as supply disruptions from Norway. However, despite the increases, abundant supply of liquefied natural gas and high levels of European reserves kept settlement prices below those registered in the first weeks of February.

As for CO2 emission rights futures in the EEX market for the reference contract of December 2024, they started the week of February 26 with a settlement price of €53.97/t, the week’s minimum. In the first three sessions of the week, prices increased to reach the weekly maximum settlement price, €57.84/t, on Wednesday, February 28. According to data analyzed at AleaSoft Energy Forecasting, this settlement price was 6.0% higher than the previous Wednesday. But in the last sessions of the week, settlement prices remained below €57/t. On Friday, March 1, the settlement price was €56.37/t, 8.0% higher than the previous Friday.

Source: Prepared by AleaSoft Energy Forecasting using data from ICE and EEX.

AleaSoft Energy Forecasting’s analysis on the prospects for energy markets in Europe and the financing of renewable energy projects

During the month of March, AleaSoft Energy Forecasting and AleaGreen are promoting their long?term price curve forecasting reports for European markets. Long?term price forecasts of AleaSoft Energy Forecasting and AleaGreen feature hourly granularity, confidence bands and up to 30?year horizons. These forecasting reports can be useful to get merchant financing and to size a PPA.