MIBEL eludes the price rises registered in the European markets in November.

In November, prices of most European markets were higher than those of October, except for MIBEL, which registered the lowest price since August 2021, including the adjustment price due to the gas cap. In most markets, the increase in wind energy production failed to offset the rise in demand and in gas and CO2 prices. The solar energy production increased compared to November 2021.

Solar photovoltaic and thermoelectric energy production and wind energy production

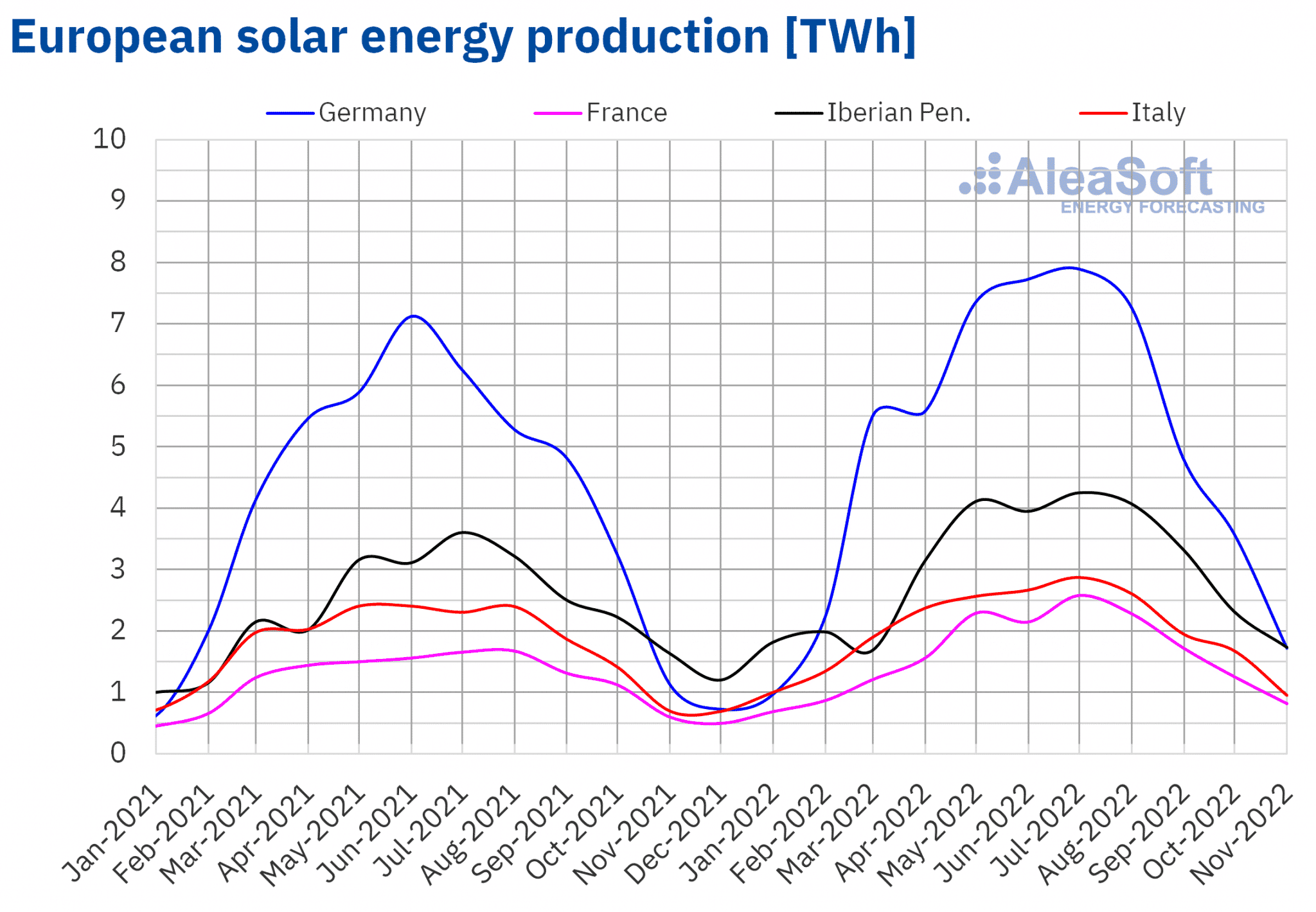

During the recently concluded month of November, the solar energy production increased compared to the same month of 2021 in all markets analysed at AleaSoft Energy Forecasting. The largest increase occurred in Germany, with a rise of 53% in year?on?year terms. The market where the lowest increase in solar energy production was registered was Portugal, with a rise of 5%.

On the other hand, the solar energy production decreased in Europe compared to the previous month, a behaviour that is in line with the decrease in hours of sunshine in the continent. The main decrease occurred in Germany, where the decrease was 50%, while Portugal was where the solar energy production decreased the least compared to October, registering a drop of 21%.

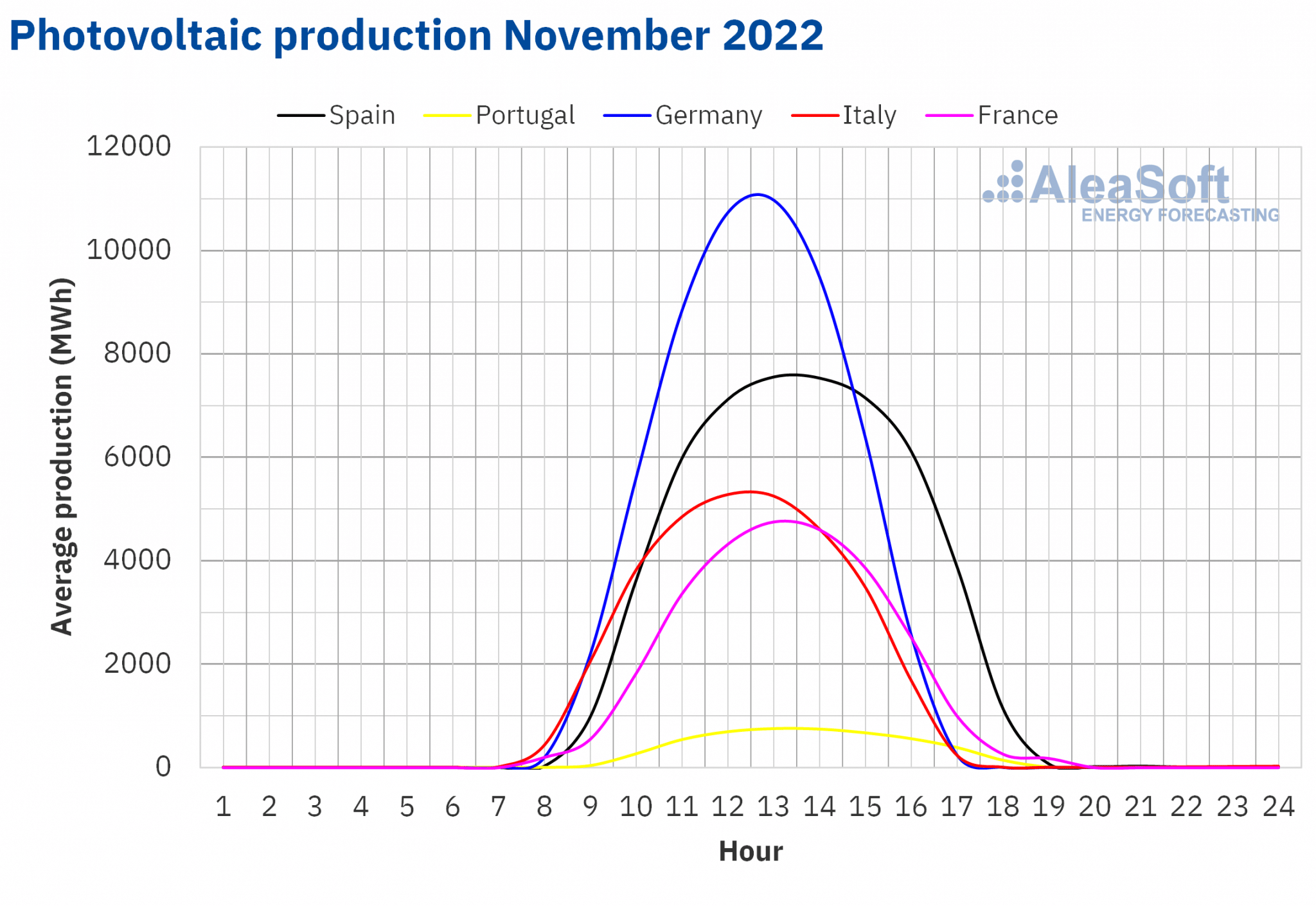

In November 2022, 167 MW of solar photovoltaic capacity were installed in Mainland Spain, bringing the installed capacity of this technology to 17 745 MW.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE and TERNA.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE and TERNA.

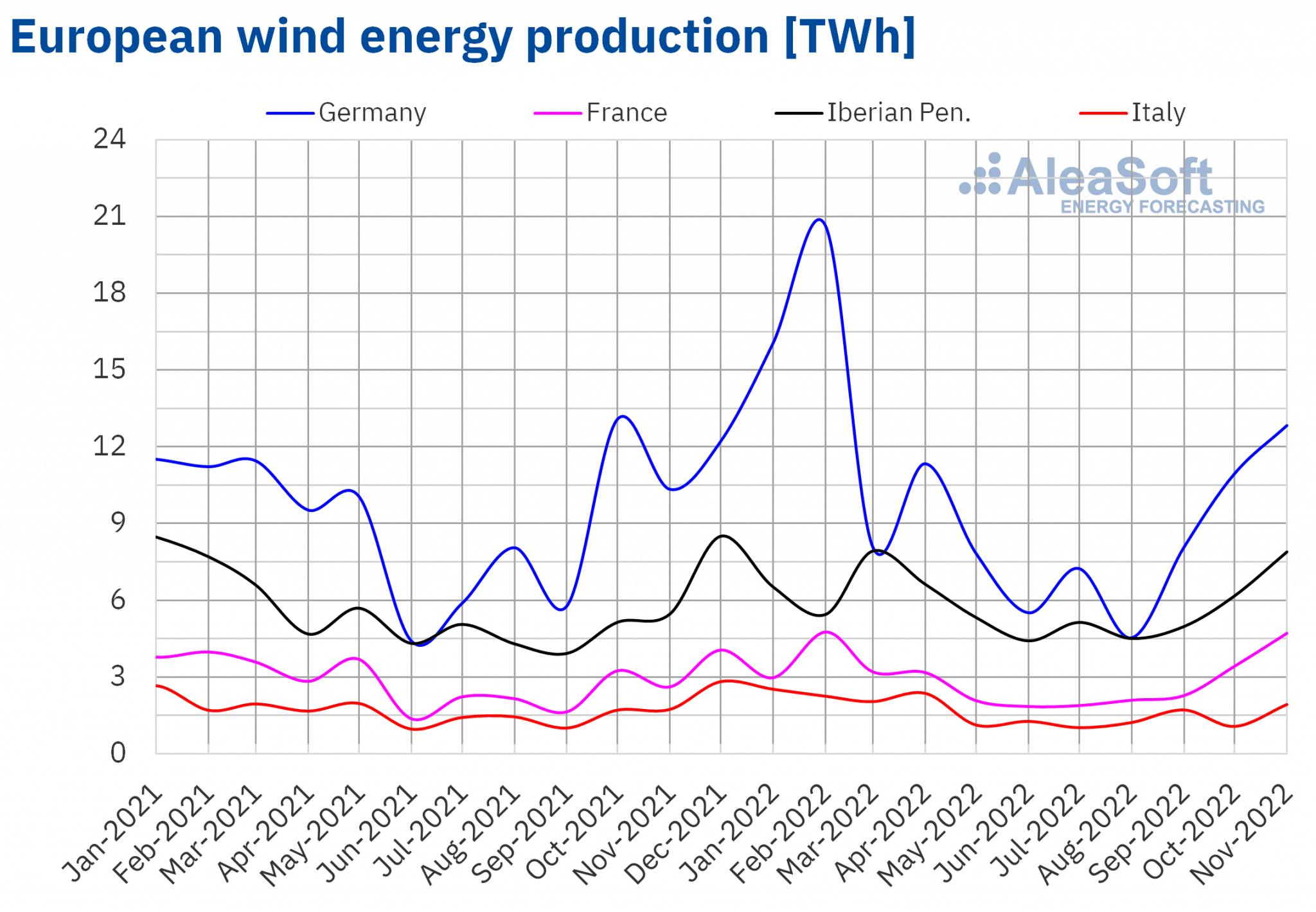

Regarding the wind energy production, the month of November ended with generalised increases compared to the same month of the previous year. This increase was most notable in France, since its wind energy production of November increased by 80% compared to that of the equivalent period of 2021. The smallest increase was registered in Portugal, of 2.0%.

The wind energy production was also higher in November compared to October, with a notable increase of 86% in Italy and Portugal being again the market with the lowest registered increase, in this case of 13%.

In November 2022, the wind energy capacity in Mainland Spain stood at 29 035 MW, with new 41 MW of this technology being installed in this period.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE and TERNA.

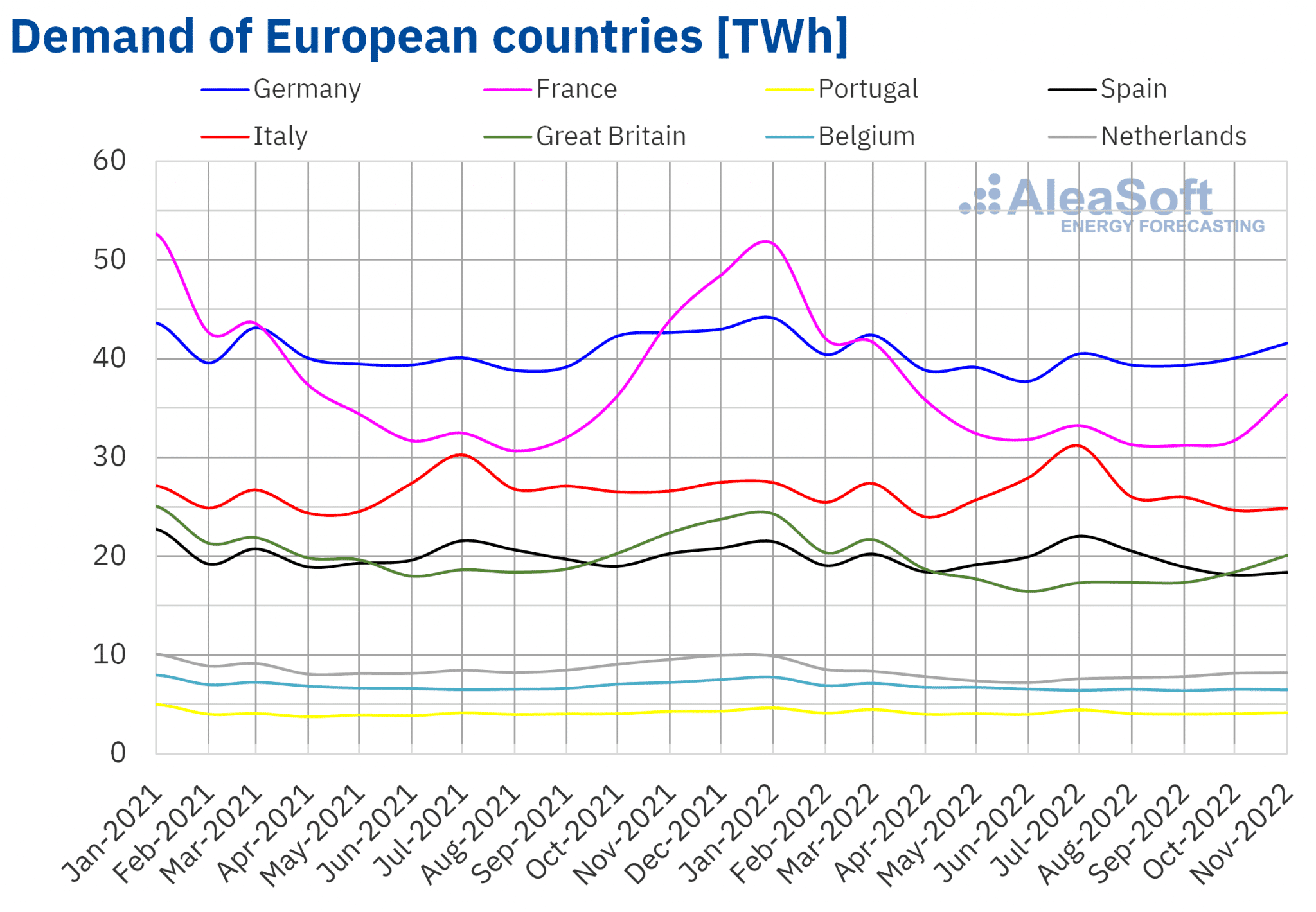

Electricity demand

In the month of November 2022, the electricity demand fell in a generalised way in the European electricity markets compared to the same month of the previous year. The largest year?on?year drop was registered in the French market, which was 17%, followed by the 14% drop in the market of the Netherlands. In the markets of Belgium, Great Britain, Spain and Italy, the decreases were between 6.6% of the Italian market and 10% of the markets of Belgium and Great Britain. The markets of Germany and Portugal were those that registered the smallest decreases, which were 2.5% and 3.2% respectively. In November 2022, the average temperatures were higher than those of the same month of 2021, which favoured the decrease in demand.

In the comparison with October 2022, the demand increased in all European markets in line with the drop in average temperatures. The largest increase was registered in the French market, which was 18%, followed by the increases of 13% in the demand of the British market and 7.3% in the German market. In the markets of Portugal, Spain, the Netherlands, Italy and Belgium, the increases were 6.2%, 5.0%, 4.1%, 4.1% and 2.4% respectively.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE, TERNA, National Grid and ELIA.

European electricity markets

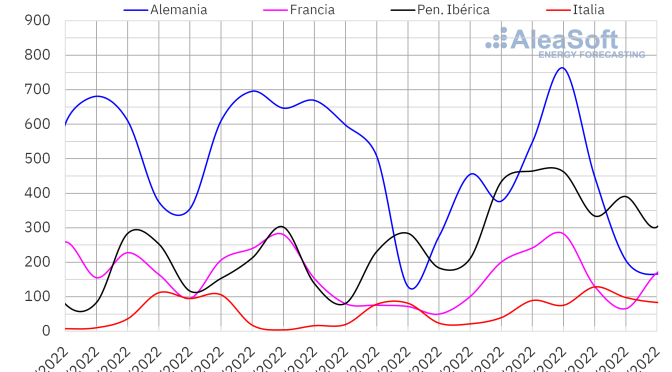

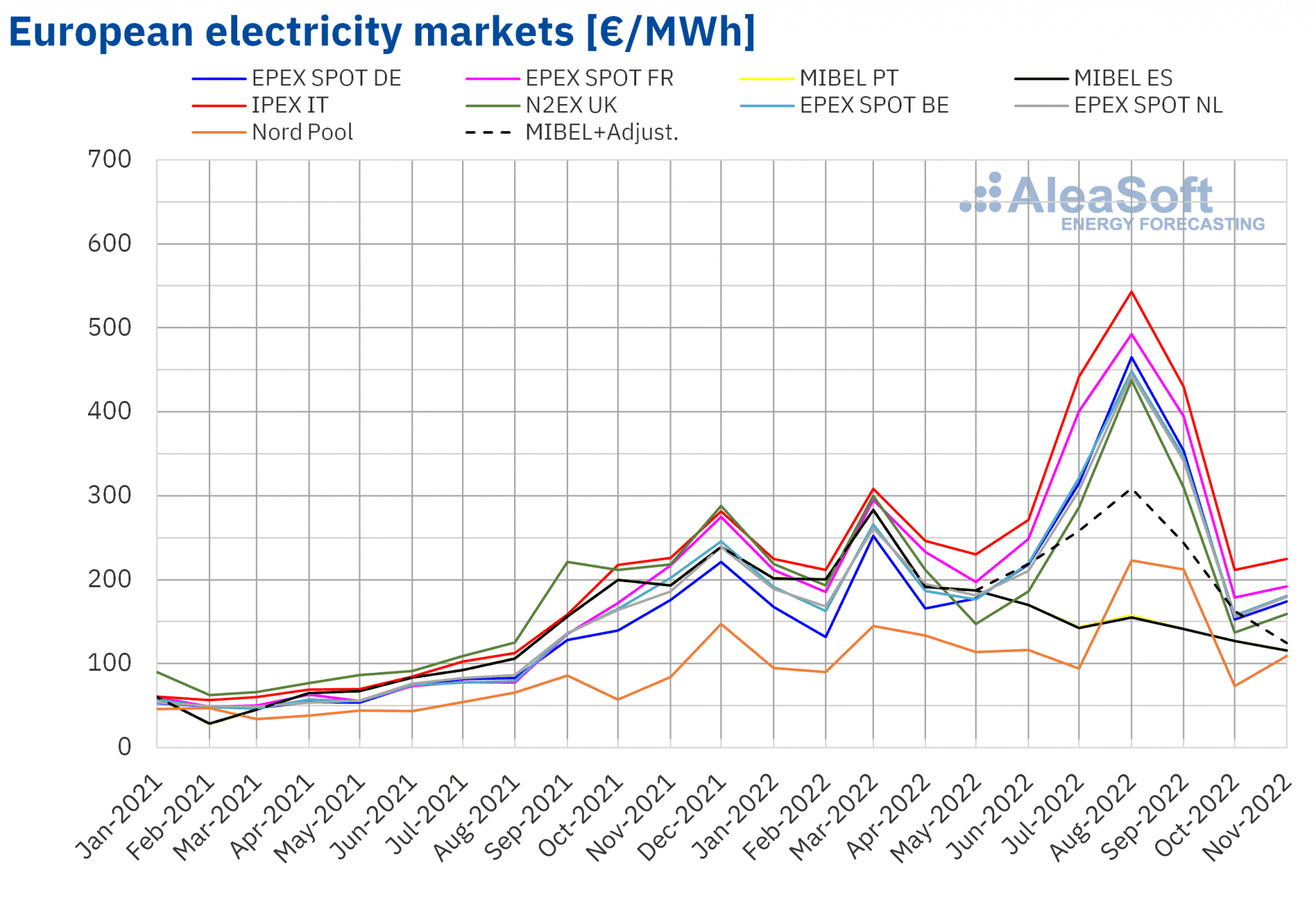

In the month of November 2022, the monthly average price was above €155/MWh in almost all European electricity markets analysed at AleaSoft Energy Forecasting. The exceptions were the Nord Pool market of the Nordic countries, with an average of €109.26/MWh, and the MIBEL market of Portugal and Spain, with €115.38/MWh and €115.56/MWh respectively. On the other hand, the highest monthly average price, of €224.51/MWh, was that of the IPEX market of Italy, followed by that of the EPEX SPOT market of France, of €191.88/MWh. In the rest of the markets, the averages were between €158.90/MWh of the N2EX market of the United Kingdom and €180.41/MWh of the EPEX SPOT market of Belgium.

In the case of the MIBEL market, if the price that some consumers have to pay to compensate for the limitation of gas prices currently in operation in this market is taken into account, the average price of November in the Spanish market was €124.43/MWh. This price is the lowest since August 2021.

Compared to the month of October 2022, in November average prices rose in almost all European electricity markets analysed at AleaSoft Energy Forecasting. The exception was the MIBEL market of Spain and Portugal, with decreases of 9.2% and 9.3%, respectively, and 24% in both cases if the price of the gas cap adjustment is taken into account. On the other hand, the highest rise, of 49%, was registered in the Nordic market, while the smallest increases were those of the Italian and French markets, of 6.2% and 7.3%, respectively. The rest of the markets had price increases between 14% of the German market and 16% of the British market.

If the average prices of the month of November are compared with those registered in the same month of 2021, prices fell in all markets, except in the Nord Pool market, where they rose by 30%. On the other hand, the largest fall in prices was that of the Iberian market, of 40%, and 36% if the gas cap adjustment price is taken into account, followed by that of the British market, of 27%. In the rest of the markets, the decreases were between 0.6% of the Italian market and 12% of the French market.

Regarding hourly prices, it should be noted that in the analysed month, hourly prices above £1000/MWh were reached in the British market on November 28 and 29, between 18:00 and 19:00. The highest price, of £1066.47/MWh, was that of Tuesday, November 29. This hourly price was the highest registered in the United Kingdom since January 24, 2022. On the other hand, during four hours of the early morning of Friday, November 11, negative hourly prices were reached in the British market. The lowest price, of ?£17.07/MWh, was registered between 5:00 and 6:00. This was the lowest price since January 3, 2022 in this market. On the other hand, on November 2, from 2:00 to 3:00, a negative price, of ?€4.10/MWh, was also registered in the Belgian market.

In the case of daily prices, taking into account the adjustment price due to the Iberian exception, on November 19 a price of €57.39/MWh was registered in the Spanish market. This price was the lowest in this market since June 20, 2021.

On the other hand, TTF gas prices in the spot market and CO2 emission rights prices increased in November compared to the previous month. This led to the increase in prices in the European electricity markets. The general increase in demand in November also contributed to the price rises. However, in the case of the MIBEL market, the increase in Iberian wind energy production and the recovery of Spanish nuclear energy production contributed to the decrease in prices.

When compared to November 2021, the general decrease in demand and the increase in renewable wind and solar energy production offset the effect of the rise in gas and CO2 emission rights prices. This led to average prices lower than those of the same month of the previous year in almost all analysed electricity markets.

Source: Prepared by AleaSoft Energy Forecasting using data from OMIE, EPEX SPOT, Nord Pool and GME.

Brent, fuels and CO2

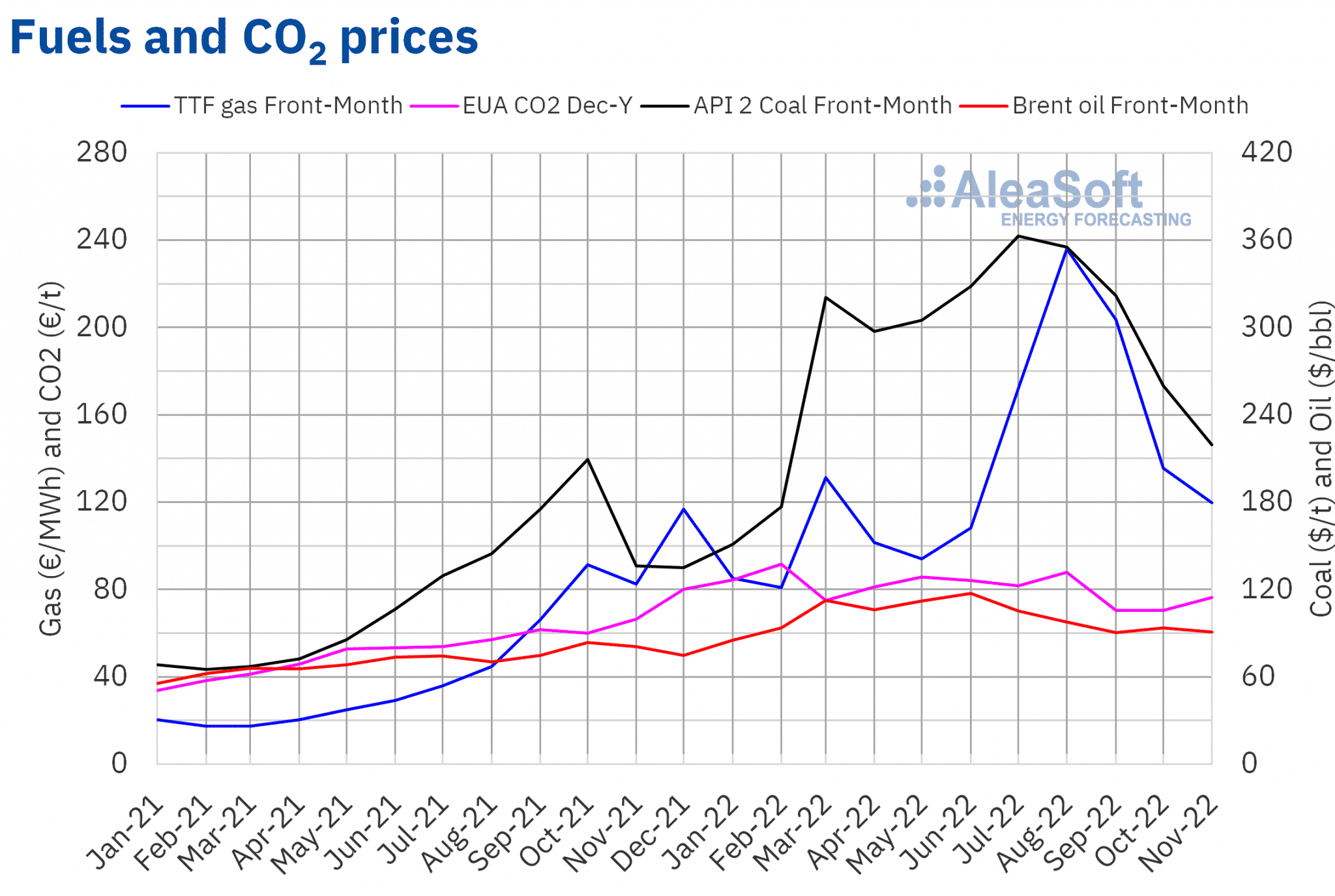

The settlement prices of Brent oil futures for the Front?Month in the ICE market fell during the month of November. The monthly maximum settlement price, of $98.57/bbl, was reached at the beginning of the month, on November 4, and was the highest since the end of August. On the other hand, the monthly minimum settlement price, of $83.19/bbl, was registered on November 28 and was the lowest since January 10, 2022.

On the other hand, these futures registered a monthly average price of $90.98/bbl in November. This value is 2.8% lower than that reached by the Front?Month futures of October 2022, of $93.59/bbl. Instead, it is 13% higher than that corresponding to the Front?Month futures traded in November 2021, of $80.79/bbl.

Concerns about the evolution of the demand due to the global economic situation influenced Brent oil futures prices downwards during the month of November. In the middle of the month, both OPEC and the International Energy Agency lowered their forecasts for 2023 demand. The spread of COVID?19 in China also contributed to increasing concerns about the crude oil demand in the second half of the month.

As for settlement prices of TTF gas futures in the ICE market for the Front?Month, in November they remained above €105/MWh, except on November 11, when the monthly minimum settlement price, of €97.85/MWh, was registered. This price was the lowest since June 14. On the other hand, in the second half of the month there were increases and the monthly maximum settlement price, of €146.40/MWh, was reached on November 30.

On the other hand, the average value registered during the month of November for these futures was €119.65/MWh. Compared to that of the Front?Month futures traded in October 2022, of €135.48/MWh, the average decreased by 12%. In addition, the average price of November was the lowest since June. But, if they are compared with the Front?Month futures traded in November 2021, when the average price was €82.56/MWh, there was a 45% increase.

During the month of November, the high levels of European reserves and temperatures higher than usual for the time contributed to the decrease in the average price of TTF gas futures compared to the previous month. However, in the second half of the month, the decrease in the number of vessels waiting to unload at the regasification plants and forecasts of low temperatures led to the increase in prices. In addition, threats of reductions in the supply of Russian gas also exerted their upward influence on prices.

Regarding CO2 emission rights futures prices in the EEX market for the reference contract of December 2022, after some fluctuations, they increased in the last part of November. These increases were influenced by prospects of low temperatures. As a consequence of this trend, on November 30, the monthly maximum settlement price, of €84.69/t, was reached. This price was the highest since the end of August.

On the other hand, CO2 emission rights futures reached an average price in November of €76.26/t, 8.2% higher than that of the previous month, of €70.49/t. If compared with the average of the month of November 2021 for the reference contract for December of that year, of €66.44/t, the average for November 2022 is 15% higher.

Source: Prepared by AleaSoft Energy Forecasting using data from ICE and EEX.

AleaSoft Energy Forecasting’s analysis on energy markets

At AleaSoft Energy Forecasting, Alea Energy DataBase (AleaApp) was developed, an online platform for the visualisation and analysis of all data from the energy markets and those variables that may have an impact on them. This tool is of great interest to data analysts, traders, energy producers and retailers, promoters of renewable energy projects, CEOs and CFOs, as well as journalists specialised in the sector, due to its reliability and ease of use, since data are compiled at the same source and with the same format.