The U.S. installed 1,330 MW of solar photovoltaics (PV) in the first quarter of 2014 to total 14.8 GW installed capacity, enough to power 3 million homes. In another significant development, Q1 2014 was the largest quarter ever for concentratesd solar power (CSP).

Key Figures

- The U.S. installed 1,330 MWdc of solar PV in Q1 2014, up 79% over Q1 2013, making it the second-largest quarter for solar installations in the history of the market.

- Cumulative operating PV capacity stood at 13,395 MWdc, with 482,000 individual systems on-line as of the end of Q1 2014.

- Growth was driven primarily by the utility solar market, which installed 873 MWdc in Q1 2014, up from 322 MWdc in Q1 2013.

- Q1 2014 was the first time residential PV installations exceeded non-residential (commercial) installations nationally since 2002.

- For the first time ever, more than 1/3 of residential PV installations came on-line without any state incentive in Q1 2014.

- Q1 2014 saw school, government, and nonprofit PV installations add more than 100 MWdc for the second straight quarter.

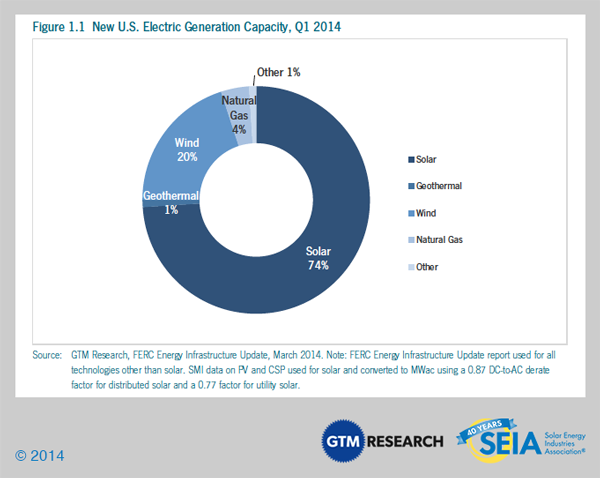

- 74% of new electric generating capacity in the U.S. in Q1 2014 came from solar.

- We forecast that PV installations will reach 6.6 GWdc in 2014, up 39% over 2013 and nearly double the market size in 2012.

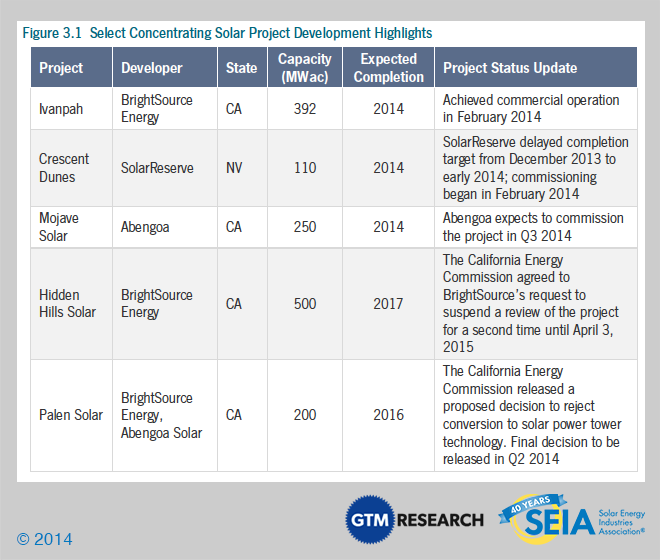

- Q1 2014 was the largest quarter ever for concentrating solar power due to the completion of the 392 MWac Ivanpah project and Genesis Solar project’s second 125 MWac phase. With a total of 857 MWac expected to be completed by year’s end, 2014 will likely be the largest year for CSP in history.

- Cumulative operating CSP capacity was 1,435 MWac as of the end of Q1 2014.

The U.S. solar market continued to expand in the first quarter of 2014. Photovoltaic (PV) installations reached 1,330 MWdc in Q1, up 79% over the same quarter in 2013. The utility PV market was responsible for the lion’s share of this growth, installing 873 MWdc in Q1 2014, up from 322 MWdc in Q1 2013. We expect this segment to fuel growth throughout the year, and our forecast calls for nearly 3.8 gigawatts (GWdc) of utility PV to be connected to the grid by December 31. To put this in context, 3.8 GWdc is more utility solar capacity than was installed in the entire history of the market through 2012. The pipeline of projects that were announced and contracted from 2010-2012 is coming to fruition now, and newer markets such as North Carolina are providing a valuable supplement to the incumbent states of California, Arizona, and Nevada. The U.S. also completed 517 MWac of concentrating solar power (CSP) in Q1 2014, more than was installed in all of 2013.

After converting the PV installations into alternating current (AC) and including CSP installations, we reach a total Q1 solar installed capacity of 1,571 MWac. This represents 74% of all new electricity generating capacity installed during the quarter.

In the distributed solar market, Q1 2014 was the first quarter in recent history in which residential PV installations exceeded commercial installations. While this is partially due to the rough winter slowing construction activity in the commercial-heavy Northeast, it is also emblematic of an ongoing trend in rooftop solar; the residential market has been slowly, steadily gaining steam for years, while the non-residential market has shown more irregular growth. The non-residential market should see stronger growth in the second quarter, once again overtaking residential installations, but our forecast now reflects our view that the residential market will be larger than the non-residential market on an annual basis as soon as 2016.

http://santamarta-florez.blogspot.com.es/2014/05/74-of-all-new-generation-in-us-came.html