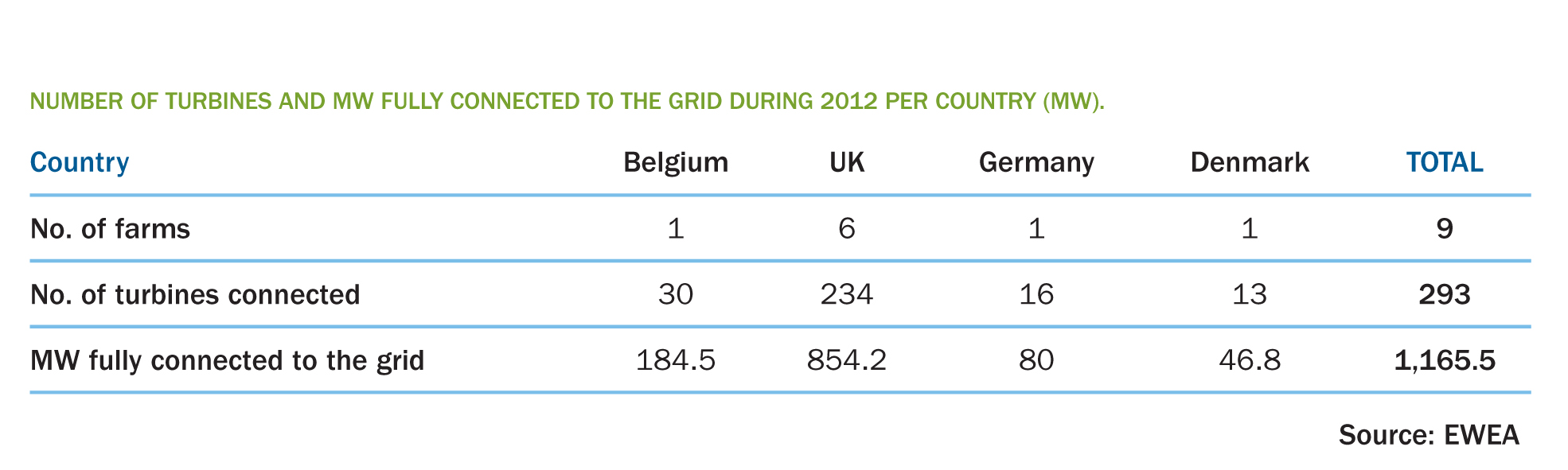

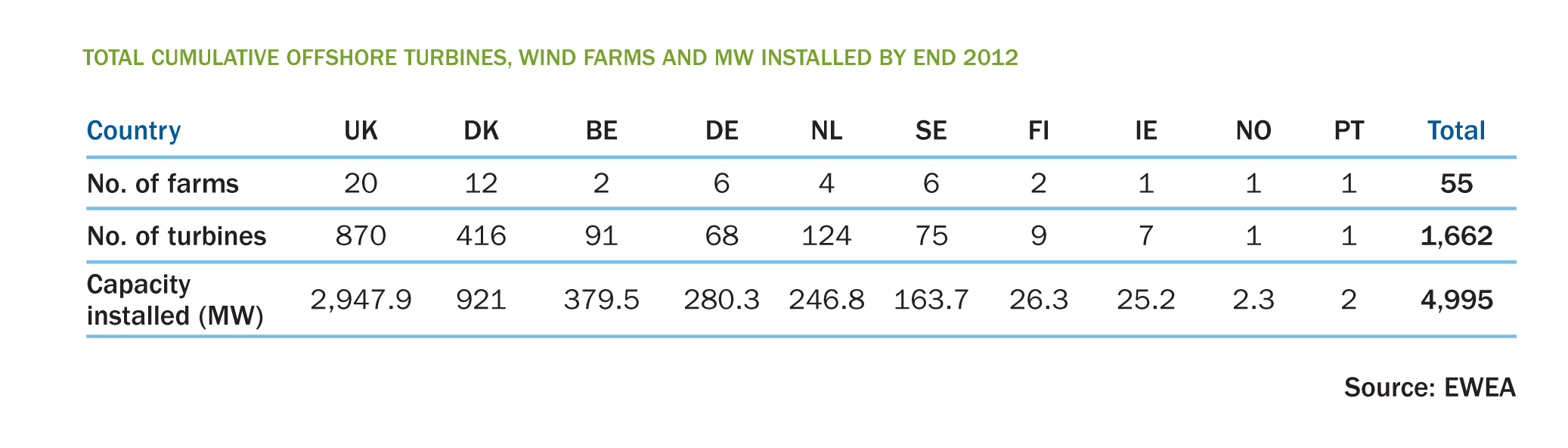

Europe installed and grid connected 293 offshore wind turbines in 2012 – more than one per working day. This brings the total to 1,662 wind turbines, in 55 offshore wind farms in ten European countries.

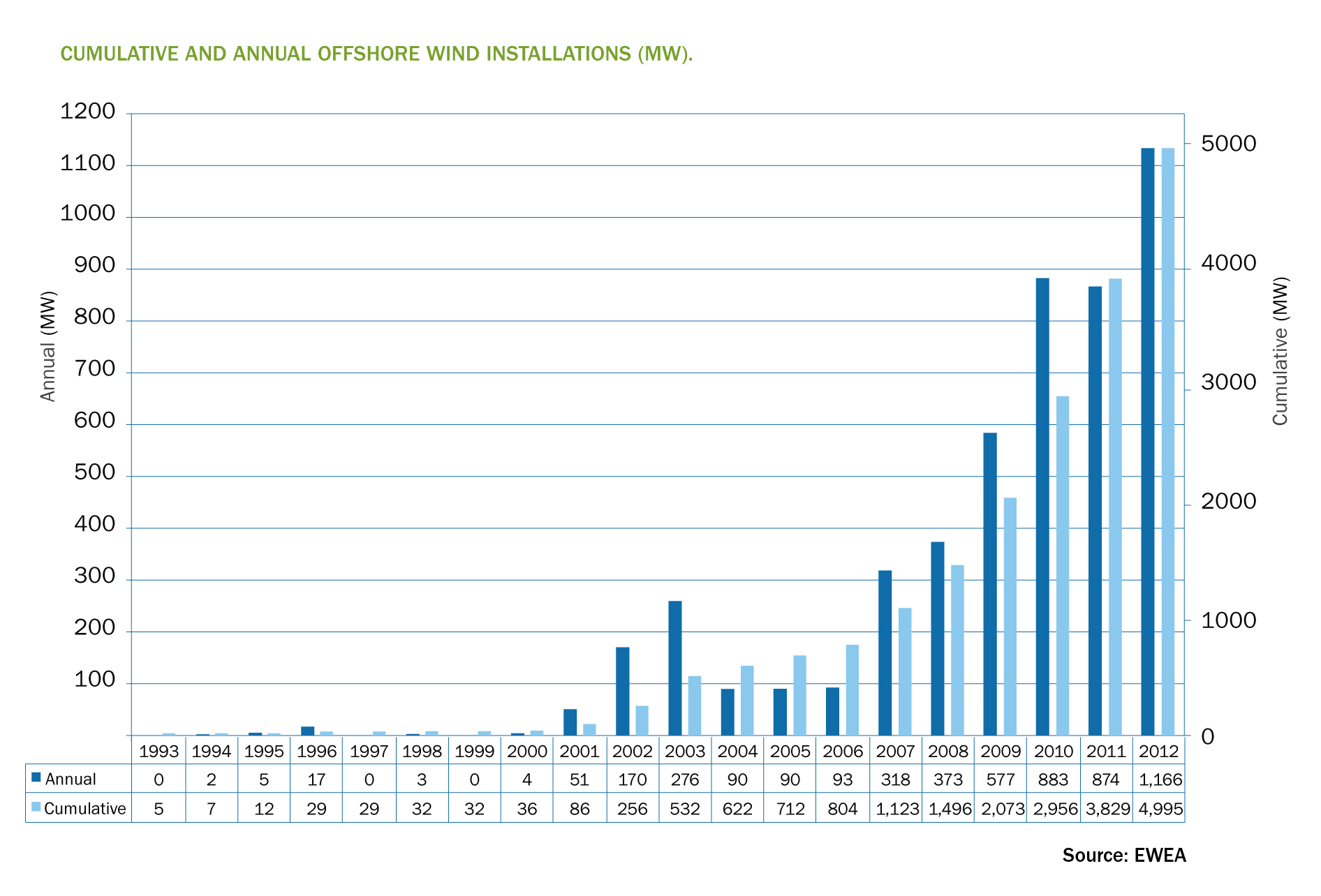

The 293 turbines installed in 2012 represent 1,165 Megawatts (MW), an increase of 33% compared to 2011 installations of 874 MW. This brings total offshore wind energy capacity to 4,995 MW. Overall, the UK remains the leader with nearly 60% of Europe’s total offshore capacity, followed by Denmark (18%), Belgium (8%) and Germany (6%).

“Offshore wind power is growing solidly”, said European Wind Energy Association (EWEA) Policy Director Justin Wilkes. “But solid installation figures do not alter the fact that the wind industry is being hit by political and regulatory instability, the economic crisis, the higher cost of capital and austerity.”

Wilkes continued: “Europe is a world leader in offshore wind energy and could be creating even more jobs if governments gave greater policy certainty to investors, and resolved grid connection problems.”

The turbines installed in 2012 represent investments of around 4 billion Euros in offshore wind farms. Offshore prospects for 2013 and 2014 are positive with 14 offshore projects under construction, due to increase installed capacity by a further 3,300 MW, and bring total offshore capacity in Europe to 8,300 MW.

293 new offshore wind turbines, in 9 wind farms, representing investments of around €3.4 bn to €4.6 bn, were fully grid connected between 1 January and 31 December 2012, totalling 1,166 MW, 33% more than in 2011.

369 wind turbines were erected during 2012, an average of 3.9 MW per day. 76 of these wind turbines are awaiting grid connection.

Work is on-going on five projects and foundation installation has started on a further nine new projects.

2012 saw Siemens as the leading turbine supplier, Bladt as the leading substructure supplier, Nexans and JDR as the leading inter-array cable suppliers, Prysmian as the leading export cable supplier, and DONG Energy as the leading developer.

1,662 wind turbines installed and grid connected, totalling 4,995 MW in 55 wind farms in ten European countries: up from 1,371 turbines, totalling 3,827 MW, at end 2011, an increase of 31%.

Overall, EU Member States are lagging behind their offshore wind energy NREAP objectives.

73% of substructures are monopiles, 13% jackets, 6%, tripods, 5% tripiles and 3% gravity based foundations. There are also two full scale gridconnected floating wind turbines, and two down-scaled prototypes.

Once completed, the 14 offshore wind farm projects currently under construction will increase installed capacity by a further 3.3 GW, bringing cumulative capacity in Europe to 8.3 GW.

Preparatory work has started on seven other projects, which will have a cumulative installed capacity of 1,174 MW.

2013 installations could be around 1,400 MW and 2014 installations around 1,900 MW.

The average size of offshore wind turbines installed in 2012 is 4 MW; it is expected that average wind turbine size will not increase significantly over the coming two years.

Average offshore wind farm size was 271 MW in 2012, 36% more than the previous year. The trend towards larger projects is expected to continue over the coming years.

The average water depth of wind farms completed, or partially completed, in 2012 was 22 metres (m) and the average distance to shore 29 km. Both average water depth and distance to shore are expected to increase over the coming years.

During 2012 a number of new generation installation vessels were delivered featuring innovative technologies, capable of operating in deeper waters (up to 75 m) and in harsher sea conditions (higher waves).

Financing activity grew faster than the sector itself during 2012. The financing pipeline for 2013 is also considerable.

In 2012, four non-recourse debt financing transactions were closed, involving almost 20 banks.

Seven equity deals were struck during 2012 and the year saw a broader pool of companies buying into the sector.

4 GW of capacity changed hands during 2012, 30% more than during the previous year.

31 companies have announced plans for 38 new offshore turbine models. 52% of new offshore turbine models announced are from European companies. Almost three-quarters of all announcements are for turbines of a rated

capacity of 5 MW or more.

1,166 MW of new offshore wind power capacity were connected to the electricity grid during 2012 in Europe, 33% more capacity than the previous year.

Over 73% of all new capacity was installed in the UK (854 MW). The second largest amount of installations were in Belgium (185 MW or 16%), followed by Germany (80 MW, 7%) and Denmark (46.8 MW, 4%).

Of the total 1,166 MW installed in European waters, 80% were located in the North Sea, 16% in the Atlantic Ocean and the remaining 4% in the Baltic Sea.

Siemens continues to be the top offshore turbine supplier in terms of annual installations. With 860 MW of new capacity installed, Siemens accounts for 74% of the market. REpower (225 MW, 19%) and BARD (80 MW, 7%) are the other two turbine manufacturers who had turbines grid connected during 2012.

Also in terms of units connected, Siemens remains on top with 239 offshore wind turbines, all 3.6 MW (82%), connected in European waters during 2012. Siemens is followed by REpower (30 wind turbines, 6.15 MW and eight

5 MW wind turbines, 13%) and by BARD (16 5 MW wind turbines, 5%).

DONG remains the biggest developer in the European offshore sector representing 19% of total installations in 2012. DONG, Statoil (12%), Statkraft (12%), RWE (9%), SSE (8%), E.ON (6%), Vattenfall (3%), Nuhma (3%) Centrica (2%), and EDF (1%) have installed over 70% of the capacity that went online during 2012.

Other developers that connected capacity to the grid in 2012 were BARD Engineering (6%), Siemens (1%, investing in the Lincs wind farm to which it supplies turbines), Enovos (1%) and marine contractor DEME (2%).

The sovereign fund Masdar (4%) and the Marguerite Fund (1%) also have stakes in offshore wind power projects.

Together, 10 power producers developed 75% of the offshore wind energy capacity that came online during 2012. In 2011 a mere five power producers were responsible for over 90% of installations.

The continued growth of offshore wind has created signifi cant opportunities across its supply chain. Substructures

represent major construction projects for construction companies. Seven companies supplied foundations to offshore wind energy projects during 2012: Bladt (193 foundations: 40% of all foundations installed) EEW (88 foundations: 18%) and SIF group (86 foundations: 18%) were the market leaders, followed by IDESA (30 foundations: 6%), CSC (24 foundations: 5%), AMBAU (22 foundations: 5%), WeserWind (19 foundations: 4%), Jan De Nul Group (16 foundations: 3%), SIAG Nordseewerk (fi ve foundations) and Aker Verdal (two foundations).

Cables – both inter-array and export – make up another signifi cant part of the offshore wind energy supply chain.

In 2012, Nexans and JDR supplied four wind farms with inter-array cables, representing respectively 21% each of the 18 wind farms. Prysmian was contracted to supply inter-array cables to three wind farms (16% of total), as was NSW (three wind farms: 16%) followed by ABB (two wind farms: 10%) and NKT (one wind farm: 5%).

In terms of export cables, in 2012 Prysmian was the lead supplier, supplying 37% of wind farms under construction.

Nexans, NKT and ABB (three wind farms, 16% each) supplied the second largest number of wind farms, followed by JDR (one wind farm).

The average capacity rating of the 293 offshore wind turbines connected to the grid in 2012 was 4 MW, 11% bigger than in 2011. The continued dominance of Siemen’s 3.6 MW turbine explains why the average size of turbines remains around the 4 MW mark.

The average size of the 18 wind farms being constructed during 2012 was 285.6 MW, 43% more than 2011. This confirms the sector’s trend towards larger turbines and bigger wind farm projects.

A total of 1,662 wind turbines are now installed and connected to the electricity grid in 55 offshore wind farms in 10 countries across Europe. Total installed capacity at the end of 2012 reached 4,995 MW, producing 18 TWh in a normal wind year, enough to cover 0.5% of the EU’s total electricity consumption.

The UK has the largest amount of installed offshore wind capacity in Europe (2,947.9 MW): 58.9% of all installations.

Denmark follows with 921 MW (18.4%).

With 380 MW (7.6% of total European installations), Belgium is third, followed by Germany (280 MW: 5.6%), the Netherlands (246.8 MW: 4.9%), Sweden (163.7 MW: 3.3%), Finland (26.3 MW: 0.6%), Ireland (25.2 MW), Norway (2.3 MW) and Portugal (2 MW).

In terms of the number of wind turbines installed in Europe, the UK is leading with 870 (52.3%), followed by Denmark (416 wind turbines: 25%), the Netherlands (124 turbines: 7%), Belgium (91 turbines: 5.5%), Sweden (75 turbines: 4.5%), Germany (68 turbines: 4%), Finland (nine turbines: 0.6%) and Ireland (seven units), Norway and Portugal both have one wind turbine each.

The 4,995 MW of offshore wind capacity are mainly installed in the North Sea (3,236 MW: 64.7%), 966 MW or 19.3% are in the Atlantic Ocean and 793 MW (15.9%) in the Baltic Sea.

There are 5,538 MW of offshore wind energy capacity installed world-wide, 90% of which is in Europe, making the region by far the world leader in offshore wind.

At the end of 2012, 509.5 MW of offshore wind energy capacity was installed in China, mainly in shallow intertidal

areas, and 33.8 MW in Japan, mostly near-shore.

12 countries across the world have offshore wind energy capacity. With almost 510 MW, China is the third biggest market behind the UK (2,948 MW) and Denmark (921 MW).

Japan (34 MW) is still only beginning to exploit its offshore potential and is the eighth biggest market, still signifi cantly behind the top seven.

Despite the growth of annual wind energy installations in 2012 and cumulative capacity almost reaching the 5 GW milestone, offshore wind deployment is lagging behind the objectives the EU Member States set themselves in their National Renewable Energy Action Plans (NREAPs), and to a lesser extent EWEA’s expectations.

In 2009, the European Wind Energy Association published a growth scenario6 that expected cumulative capacity in the EU to overtake the 5 GW mark during 2012. Eight EU Member States indicated in their NREAPs – submitted to the European Commission as required by the Renewable Energy Directive7 – offshore deployment objectives that, taken together, add up to over 5.8 GW at end 2012.

In terms of number of wind turbines installed at the end of 2012, Siemens remains the top supplier with 940 turbines. Vestas has installed and grid connected 533 turbines representing 32% of total installations, followed by REpower (74 turbines: 4%), BARD (32 turbines: 2%), WinWind (18 turbines: 1%), GE (14 turbines: 1%) and Areva with six wind turbines.

Please find essential graphs here:

The number of turbines fully grid connected by country in 2012

{kind=link}

Total cumulative offshore turbines, wind farms and MW installed by end 2012

{kind=link}

Cumulative and annual offshore wind installations 1993-2012 by MW

{kind=link}